In its ten year forecast, FTI Intelligence believes 82.7% of new capacity (570.4GW) added between 2018 and 2027 will be added in just 15 markets: China, US, India, Germany, France, UK, Brazil, Mexico, Turkey, Japan, Netherlands, Argentina, Spain, Taiwan and Canada.

FTI predicts 689GW of new wind capacity will be added in these countries over the next decade, meaning less than 120GW will be installed in the rest of the world.

This echoes the trend from 2017, which saw 89% of new capacity added in just ten markets, according to figures from the Global Wind Energy Council (GWEC).

| Country | Total Installations 2018-2027 (MW) |

| China | 296,000 |

| US | 65,500 |

| India | 44,000 |

| Germany | 40,205 |

| France | 19,400 |

| UK | 16,870 |

| Brazil | 16,500 |

| Mexico | 11,500 |

| Turkey | 11,150 |

| Japan | 9,730 |

| Netherlands | 8,800 |

| Argentina | 7,900 |

| Spain | 7,800 |

| Taiwan | 7,555 |

| Canada | 7,500 |

| Rest of the World | 118,590 |

| TOTAL | 689,000 |

Source: FTI Intelligence

While this does suggest a slight diversification over the next decade, FTI’s figures cannot take into account policy changes.

Should just one of the top 15 markets take a sharp downturn, there could be repercussions across the whole industry.

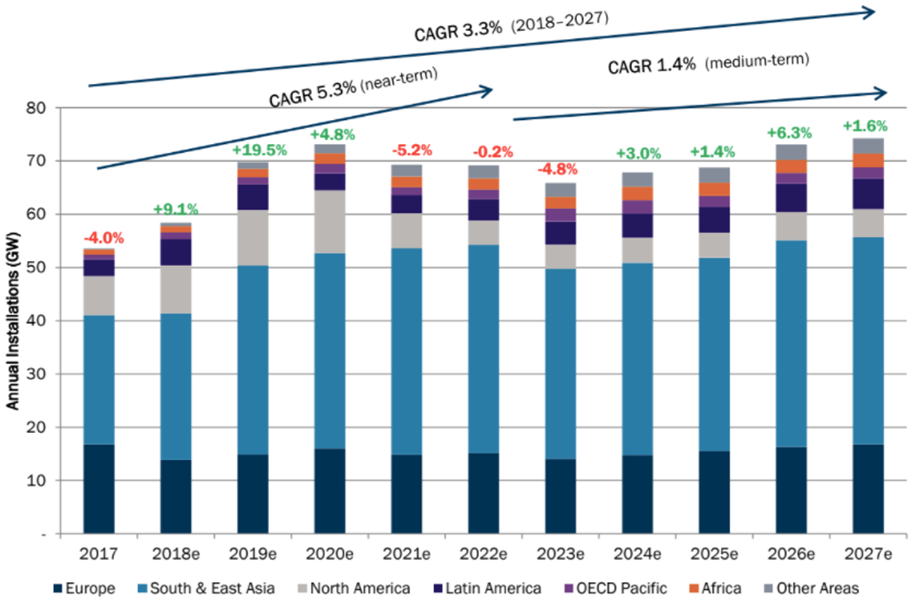

Over the next decade, FTI believes global wind capacity will grow at a compound annual growth rate (CAGR) of 3.3%.

In the near term (2018-2022), CAGR could be as high as 5.3%, with the Chinese market remaining vital to global growth.

Beyond this, however, in the medium term (2023-2027) CAGR could fall to just 1.4%.

Much of the difference in CAGR coincides with the expiration of the production tax credit in the US, reducing North America’s growth beyond 2021.

The Asia-Pacific region, particularly China, is expected to install 55.4% of the new capacity over the period, while Europe, the Middle East and Africa (EMEA) will add 28.3% and the Americas will add 16.3%.

FTI predicts China to come back in a big way in 2018, following a slowdown in 2017.

This year, FTI believes onshore installations worldwide will grow by 9.1%. However, excluding China, the rest of the world will see a 1.5% increase in the onshore sector.

The relatively small offshore market will continue to grow over the decade, with a CAGR of 10% aided by more markets joining the sector, notably France and Taiwan. China is predicted to become the largest offshore market by installed capacity in 2021, surpassing the UK’s total.

.png)

HR.jpeg)

.png)