Question: Is buying from a conglomerate safer or more appealing, and why?

Lars Weber, sales manager of renewables, Neas Energy

In delivering renewable energy projects, the major focus point for investors and debt providers is security of income. This income is relying on two parts, the income per megawatt hour and the amount of magawatt hours generated by the turbines.

In delivering renewable energy projects, the major focus point for investors and debt providers is security of income. This income is relying on two parts, the income per megawatt hour and the amount of magawatt hours generated by the turbines.

To secure the income per MWh, investors are relying on the strength of the support scheme together with the power purchase agreement that an offtaker can offer. For the amount of MWh, the investor has to rely on the turbines and in case that these fail, the guarantees that the manufacturer of the turbines can offer.

Guarantees for turbines' performance are only as good as the counterparty that underwrites these. Therefore, the counterparty strength of the turbine manufacturer is vital. If the turbines' manufacturer were no longer be available, the guarantee would be worthless and the security around the amount of MWh that will be generated diminishes.

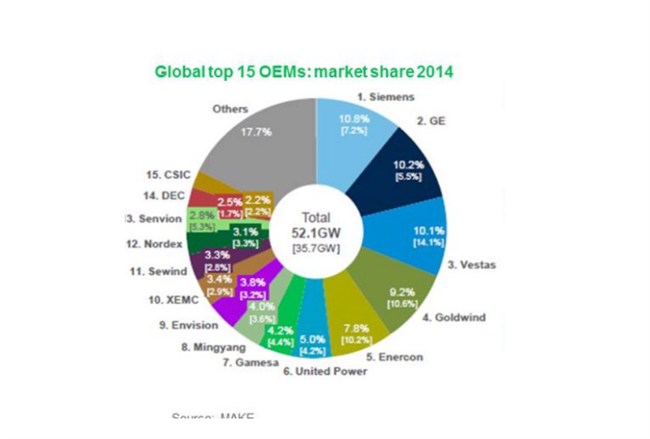

Conglomerates are larger entities than specialised turbines manufacturers. Therefore, their counterparty strength is larger and their guarantees are perceived as safer. A prudent investor is therefore valuing a performance guarantee from a conglomerate higher as there is a higher chance it can be enforced. This perceived security gives conglomerates an edge over the specialised turbines manufacturers.

Philip Totaro, founder and CEO, Totaro & Associates

At this stage of the wind industry's maturity there is much greater sensitivity to both Capex and Opex costs, so the lowest purchase price for a given availability guarantee is what has driven recent sales in most markets. Higher fleet-wide availability and scale of operations are two appealing factors driving interest in equipment supply from conglomerates.

At this stage of the wind industry's maturity there is much greater sensitivity to both Capex and Opex costs, so the lowest purchase price for a given availability guarantee is what has driven recent sales in most markets. Higher fleet-wide availability and scale of operations are two appealing factors driving interest in equipment supply from conglomerates.

Additionally, conglomerates offer global reach and the ability to access capital in existing as well as emerging markets, the global scale of their supply chain, the balance sheet strength, as well as their brand reputation to stand behind their products has been a draw for investors as well as turbine purchasers. The finance community and project developers now prefer consistency and the stability they seem to offer.

Several major conglomerates have recently announced deals in which wind was simply one component of their overall scope of equipment supply as well as services. Smaller regional players that have not been able to globally diversify their sales pipeline will be faced with the prospect of exiting the market or partnering with other regional firms as they struggle to find revenue from sales or services.

Additionally, we are likely to see more interest in the acquisition of the regional players by conglomerates that are seeking to enter the wind market to compliment their existing product and service portfolio in energy.

.png)

.png)