The long-recognised potential for wind power in Latin America is now being realised on an industrial scale. Across the region — and not only in the established hotspots of Brazil and Mexico — wind projects are being planned and permitted, constructed and commissioned at a rate of growth way in advance of that currently seen in North America or Europe. Wind power's expansion is being driven by good wind resources and land availability, together with largely supportive governments responding to increasing demands for energy from their growing economies.

The potential in the region is such that it is easy to forget that it remains a very modestly sized market. At the end of 2013, even after another 12 months of rapid growth, total installed capacity in the whole of Latin America — at a shade under 6GW according to “uåX˜äŠÊ˜·³Ç Intelligence — was less than half that provided by the US state of Texas alone, for example, or less than one fifth of that installed by Germany. On a global scale, the region is still a small player.

But that position will change quickly over the next few years, according to industry observers. An assessment of the Latin-American wind market, published by Navigant Consulting in late 2013, forecasts the addition of more than 3GW of installed capacity annually over the next ten years. By the end of the decade that would take its total installed capacity close to 30GW, nearly five times the current size.

Navigant's optimism is backed up by “uåX˜äŠÊ˜·³Ç Intelligence figures, which indicate that some 9GW of wind projects being planned are well advanced, with site permitting completed and with power purchase agreements (PPA) and turbine purchase agreements (TPA) in place. In many cases, construction is already well under way. The longer-term pipeline, measured by sites having been acquired and the permitting process started, looks healthy too at around 30GW.

For US and European manufacturers and developers, Latin America looks an increasingly safe haven in which to diversify their portfolios, especially with Chile, Costa Rica, Uruguay, Peru and Panama joining the bigger players in developing wind power on a utility scale.

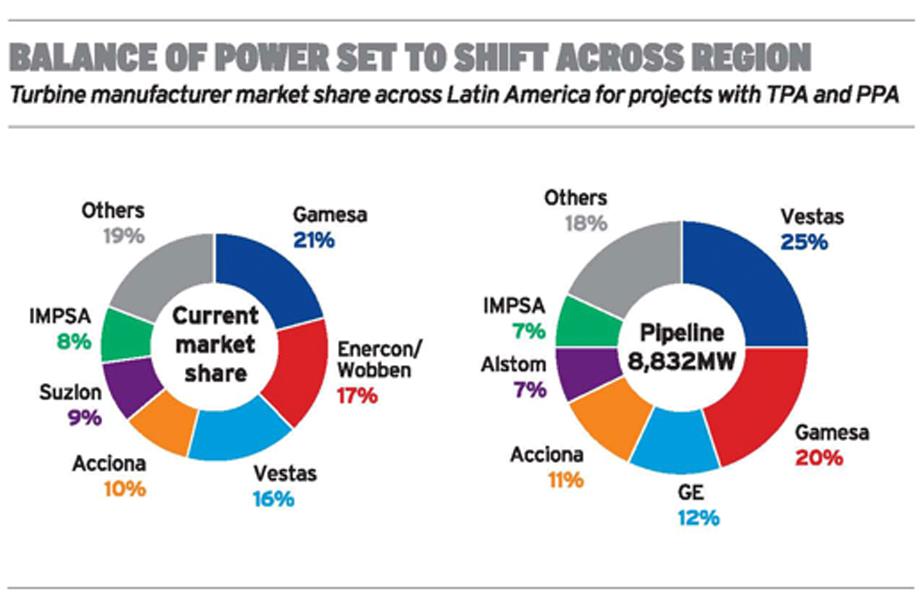

Market share

Brazil's strict local content rules - turbine makers must source 60% of their hardware from within Brazil to secure favourable finance from the state-owned Brazil Development Bank - restricts the number of manufacturers in the region. The qualified companies are: Alstom, Acciona, Enercon/Wobben, Gamesa, GE and IMPSA, although Vestas has announced plans to meet the local content requirement shortly.

Gamesa leads the Latin-American market as a whole, with 21% of current installed capacity, mostly in Mexico, where its G90-2.0MW has been the turbine of choice for several years. Enercon/Wobben stands at 17%, thanks to the popularity of its E82-2.0MW machine in Brazil.

However, the “uåX˜äŠÊ˜·³Ç Intelligence pipeline figures suggests a shift in the balance of power, with Vestas and GE in particular strengthening their presence. Vestas has 25% of the pipeline capacity with TPAs in place, ahead of Gamesa (20%) and GE (12%).

.png)

.png)