The original target of over 5GW by 2015 was set as part of the country's five-year plan. WPO Intelligence figures show that by the end of 2016, China will have installed a total of 3.9GW offshore, a 44% decrease on the previous year's 2016 cumulative offshore target of 7.1GW.

Speaking at a Sino-British conference dedicated to offshore wind case studies and technology exchange, Shi Lishan, deputy chief of new and renewable energy division at the National Energy Administration, said there would be "a degree of difficulty" in hitting the 7.1GW target. China has been among the early adopters of offshore wind with around 320MW demonstration projects online, however it has yet to build a commercially-backed project.

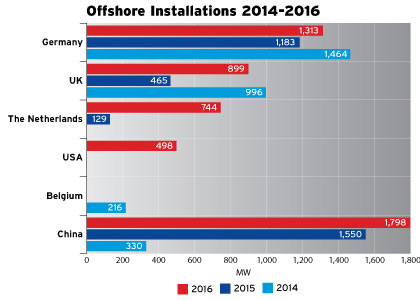

Elsewhere, the UK and Germany will stay way ahead of other countries in terms of offshore installations over the new two years. The Netherlands will come a distant third, well in front of the US, which will take fourth place — if Cape Wind goes ahead.

If all goes to plan, German installations in 2014 will be higher than those of the UK. According to WPO Intelligence, Germany is set to install 1.4GW by the end of this year, with completed projects including Dan Tysk (288MW), Global Tech 1 (400MW) and Borkum West 2 (200MW).

In comparison, the UK is set to install just under 1GW. The bulk of this capacity is at Gwynt y Môr (576MW), which came online this week, and West of Duddon Sands (389MW), which finished turbine installation last month. The remaining UK installations this year consist of demonstration projects.

Projects sizes in Europe are growing, but perhaps not quite as much as had been anticipated. Currently, the average project size in UK waters, excluding small sub-20MW demonstrator projects, is about 250MW. Of those set to come online by 2016, sizes start at around 400MW. German projects over the three-year period studied remain under 300MW.

Elsewhere, the Netherlands is set to install 873MW between now and the end of 2016, with Eneco Luchterduinen (129MW) to come online in 2015 and Gemini (600MW) and Westermeerwind (144MW) due in 2016.

.png)

.png)