As of the end of 2018, Europe’s total installed wind capacity was 189.2GW, following the new capacity and 421MW of decommissionings. There is offshore.

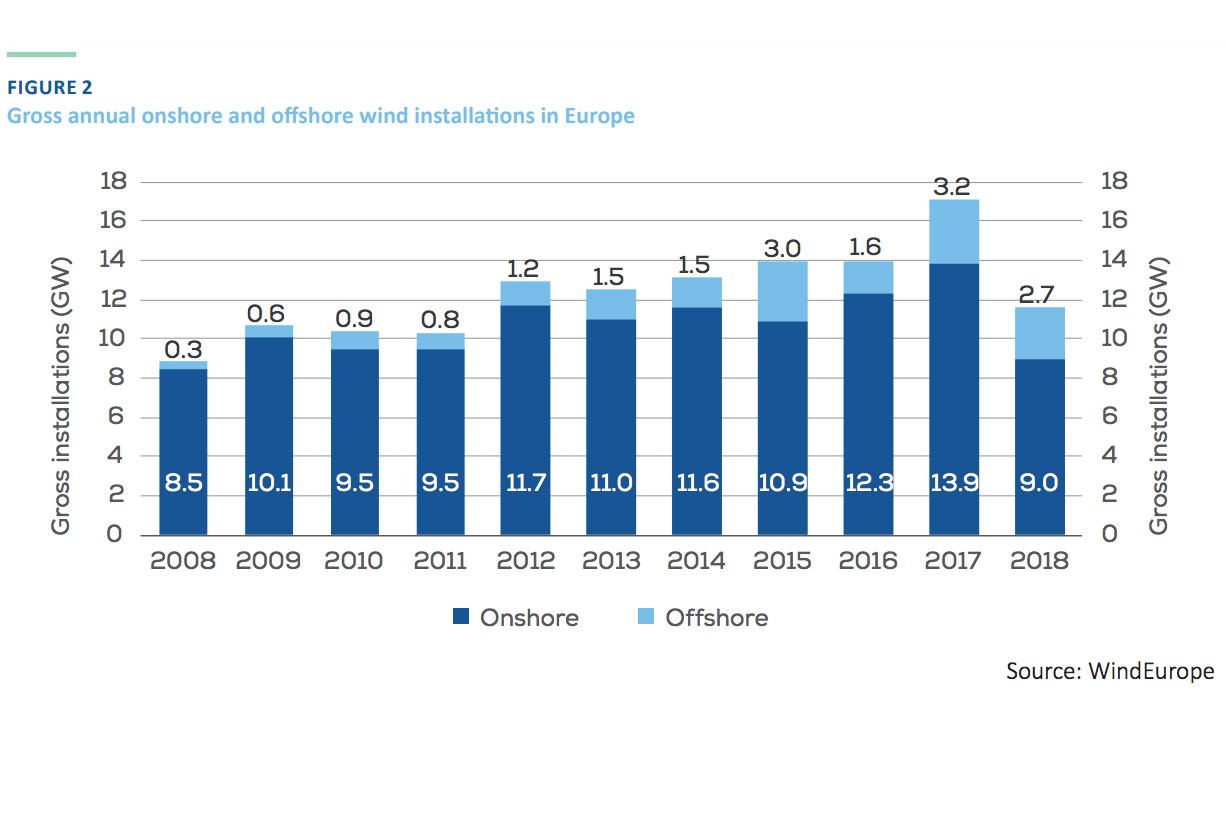

Among the EU-28 members, gross installations fell to 10.1GW, the lowest level since 2011, WindEurope said.

This "reflects regulatory changes that European Member States have undertaken since the review of the European State-Aid Guidelines", the lobby group said.

"This has led many countries to introduce auctions since 2016, creating a new environment for permitting and project development, resulting in a slowdown."

Approximately 68% of Europe's total wind capacity is installed in just five countries.

Germany continued as the leading market, but saw a significant drop-off. Roughly 3.37GW was added last year, including 969MW of offshore capacity, down from a total of over 6.5GW in 2017.

Onshore totals more than halved year on year to 2,402MW as "a consequence of lengthy permitting processes and citizens’ projects that were granted longer build-out periods", WindEurope said.

The UK, the region’s second-largest market, also witnessed a dramatic fall in additions. It added 1.9GW last year, down from 4.27GW with the near-collapse of its onshore market.

France was the third largest, with relatively flat onshore additions of 1,565MW for 2018. However, its apathetic offshore industry is holding its growth back.

No other market surpassed 1GW of new capacity in 2018, despite rising concerns about the world’s climate.

Fourteen countries did not add any new capacity, 12 of which are EU member states.

"Last year was the worst year for new wind energy installations since 2011. Growth in onshore wind fell by over half in Germany and collapsed in the UK.

"And 12 EU countries didn’t install a single wind turbine last year," said WindEurope CEO Giles Dickson.

"There are structural problems in permitting, especially in Germany and France. And with the noble exception of Lithuania, and despite improvements in Poland, there’s a lack of ambition in Central and Eastern Europe.

"The 2030 National Energy & Climate Plans are a chance to put things right. But the draft Plans are badly lacking in detail: on policy measures, auction volumes, how to ease permitting and remove other barriers to wind investments, and how to expand the grid.

"Governments need to sort this out before they finalise the plans this year," Dickson added.

The disappointing year for capacity additions followed a widespread shift to auctions and tenders.

WindEurope noted 9.3GW of potential capacity was produced across these competitive processes in eight countries.

On a brighter note, 16.7GW worth of projects reached Final Investment Decisions in 2018: 4.2GW offshore and 12.5GW onshore wind. This compares to 11.5 GW in 2017.

Generation

The bloc's wind capacity generated 362TWh of electricity in 2018, enough to supply 13.7% of Europe's demand.

Wind's share in final electricity share increased by two percentage points, WindEurope said, but partly as a result of a lower demand.

Wind production in Denmark achieved a 41% share of electricity demand, followed by Ireland (28%), Portugal (24%), and Germany (21%). In a further five markets, wind covered over 10% of demand.

WindEurope noted 2018 was a "less windy year than 2017... reflected in a decrease of the capacity factors for onshore (22%) and offshore (36%)".

.png)

HR.jpeg)

.png)