Financial results for H1 reported DKK 2.8 billion (€375 million) net profits, compared with DKK1.4 billion for the same period last year.

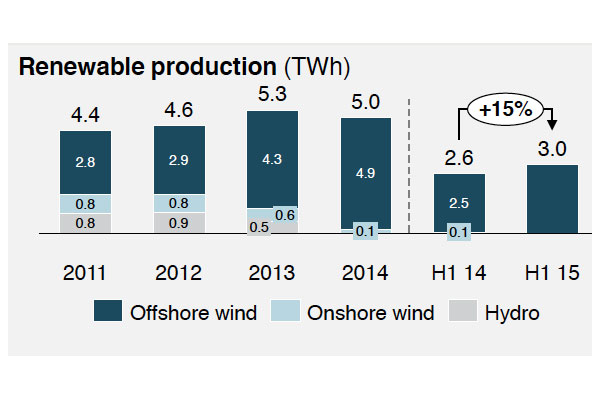

Production from its wind projects, now all offshore, delivered 3TWh in January to June 2015, an increase of 15% on the same period last year. The company attributes this to the 389MW and 210MW projects both coming fully online, and the company's purchase of the remaining 50% share in the 90MW Barrow wind farm, all in the UK.

This was countered by production loss from the divestment of 25% of the 630MW London Array project last year, leaving Dong with 25% ownership. A one-month cable failure from Anholt in Denmark also reduced production, incurring financial losses that are compensated by the transmission provider.

While revenues are up year on year, wind’s EBITDA fell by 31%. This was due to a particularly high first half of 2014, following the sales of 25% of London Array and 50% of Westermost Rough, the latter in line with the company’s strategy of 50/50 shares in projects. "You can expect us to continue this strategy," Dong CEO Henrik Poulsen said of future ownership arrangements for offshore projects.

On the back of these results, the company has revised its outlook upwards for the remainder of 2015, now expecting an EBITDA of DKK 17-19 billion (€2.27-2.54 billion), up by DKK1.5 billion.

The company’s plans to increase wind power expansion is unchanged, with the 312WM Borkum Riffgrund 1 in the German North Sea next for completion, and the first US project on the furthest horizon.

When asked about continued financial support for UK projects, Poulson said: "It is hard for us to speculate about specific amounts, but we think there is still solid support from the government."

.png)

.png)