Offshore wind remains the single largest potential contributor to most major European economies meeting their 2020 renewable energy targets. With approximately 4GW of generation capacity installed to date across 53 wind farms in ten European countries, offshore wind is expected to drive an additional €100-150 billion of investment to reach a projected capacity of up to 40GW by the end of the decade. Large programmes, in the UK and Germany in particular, underpin further developments for decades beyond 2020.

This rapid growth plan is not without delivery issues — technical viability, affordability and financing to name a few. We see four major challenges for the industry:

A techno-economic challenge, with a pipeline of projects that exhibit different technical characteristics across the board and, with them, different needs and deployment rates

Financing that, to date, has come primarily from utility sponsors, whose balance sheets are stretched

Grid infrastructure procurement for which the traditional delivery model seems inadequate

Policy — governments struggling to put in place the right framework to unlock investments over the long term.

The techno-economic challenge

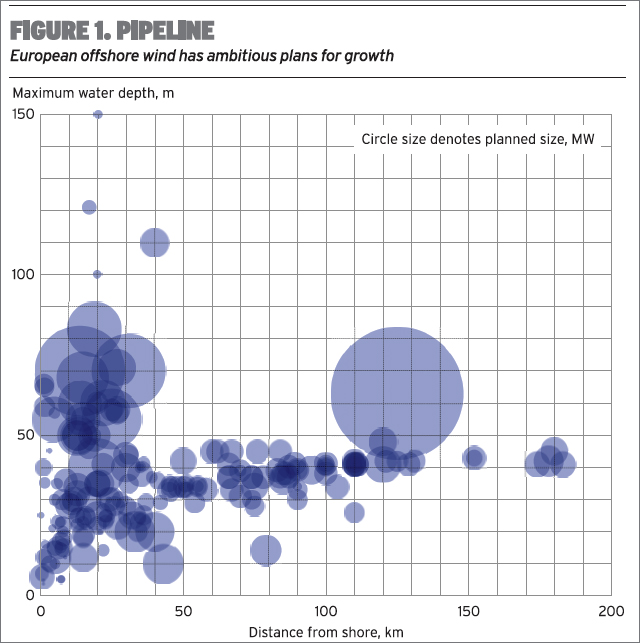

The offshore wind pipeline in Europe, if we include only projects that are truly ‘in progress’, albeit at a very early stage of planning in some cases, consists of about 200 wind farms. These can be thought of as three broad segments, differentiated by their respective technical characteristics and feasibility, and therefore current economic viability (see Figure 1).

The most advanced — and economically viable — pipeline segment, which totals some 19GW (c. €60-80 billion), is the by-product of a series of national programmes that target offshore wind deployment in locations close to shore (within 50 kilometres, say) and in shallow waters up to 30 metres deep.

This consists of projects with an average project size of just under 300MW that can be delivered under the techno-economic paradigm: using ‘conventional’ and ‘tried and tested’ technologies, foundations and construction techniques. With steady improvements and standardisation in the engineering, procurement and construction of these projects, as well as in operating track record, this market segment is showing promising signs for delivery at costs of £100/MWh (€125/MWh) by 2020.

Most of that deployment, however, hinges on the financial strength — and to some degree, engineering knowhow — of just a few utility majors, whose balance sheets are constrained. Managing construction and long-term operating risks will be areas of great focus for these sponsors, who will increasingly be relying on third-party capital to finance construction, or recycle capital post-construction by sharing their long-term hold.

The second market segment is a fraction more challenging: operating further from shore increases the logistical challenges of construction and operation and maintenance. While this might be partly offset by the greater wind resource, these projects are inevitably proportionally more expensive to deliver by virtue of the cost of the grid infrastructure required to connect them to shore. This segment at present represents some 10-15GW of capacity and will only be delivered if viable techno-economic models can be developed. We do not envisage delivery of much of that capacity before 2020.

The third and largest market segment is potentially significantly more challenging and costly to deliver with existing techniques, with average project size likely to exceed 500MW. Greater water depths require much larger foundations, which in turn accommodate larger turbines. The realisation of this pipeline of projects, in our opinion, hinges on technology innovation and policy. Policymakers in particular will have to ensure they can keep the market incentivised to take development risks and make significant R&D investments to ensure that a viable techno-economic model can be delivered, in turn ensuring value for money for the consumer. This will require political leadership and long-term commitment.

The financing challenge

Over the past decade, the credit rating of the 11 largest utilities involved in offshore wind projects has been reduced from an average of A+ to A-/BBB+ (See Figure 2). While this is still investment grade, the credit quality of the sector has become much more segregated due to the aftermath of the financial crisis and infrastructure renewal needs.

In practice, this means that the cost of capital for these utilities is increasing, reflecting ‘greater risk’ for investors holding corporate debt or equity instruments in these businesses. Such sponsors are now actively seeking opportunities to partner with other trade or financial institutions that can provide liquidity and/or knowhow to mitigate development, construction or long-term operating risks. Various sources of third-party debt or equity capital are being considered.

There are at present approximately 15-20 banks with lending appetite for the offshore wind sector. Their motivations are not limited to securing higher margins. Banks are also motivated by softer considerations, such as strategic interest to gain expertise in an up-and-coming sector expected to require significant amounts of capital going forwards, or a desire to maintain or secure relationships with key clients. This is the case, for example, for utility sponsors and service providers.

Given the lenders’ general reluctance to be exposed to any construction risks — which can hardly be underwritten by large EPC providers on commercial terms in today’s market — utilities often find it cheaper and easier to finance the construction of these projects on their balance sheet initially, with the objective of refinancing post-construction. Despite increasing refinancing costs, and lending margins shooting up to 250-350 basis points (or 2.5-3 percentage points) above the base rate, all-in rates for debt have actually remained relatively stable due to the low-interest environment.

Raising project finance can be a cumbersome exercise too. With an average hold of €50 million-€75 million, it can take up to ten banks to finance a typical 300MW offshore wind farm. Getting that consortium of lenders to bed down all issues and agree to a common financing framework is often a lengthy process (12-18 months) which drives stringent diligence procedures and a high level of structuring. Key contracts need to be backed up by blue-chip counterparties and provide security to lenders for the duration of the loan (up to 15 years) by way of long-term power offtake, operation and maintenance arrangements, appropriate construction guarantees and suitable long-term warranty provisions.

Assuming each commercial bank can participate in one to two deals per year, there is approximately €1.5 billion in commitments available for offshore wind from the commercial markets in Europe annually. With billion-sized transactions becoming the norm, this can only realistically allow for a couple of transactions to be closed in Europe per year. The lack of liquidity for these types of assets today remains significant.

Export credit agencies

Since 2006, 11 project-finance transactions have closed in Europe, mainly in the UK, Belgium and Germany. The participation of multilateral agencies and export credit agencies (ECAs) has to date been critical to enable commercial lending into these projects by providing liquidity, credit worthiness and credibility (see Figure 3).

The European Investment Bank (EIB) has been most active, channelling more than €2 billion into the sector to date. Significant commitments are expected in the next few years from Germany’s KfW, through its Offshore Wind Energy Programme, and the UK’s Green Investment Bank, with up to €5 billion and £3 billion respectively.

ECAs play a major role as providers of funding and credit enhancement. However, their involvement is limited to support of national exports and therefore availability of support linked to the choice of equipment used. Denmark’s EKF and Germany’s Hermes have been particularly active.

Multilaterals and ECAs typically take up to 50% of the risk or funding of a transaction. Assuming approximately €1.5 billion is available from commercial lenders each year, and that this can be match-funded by multilaterals, there is some €3 billion of senior debt capacity for projects in Europe. Assuming a debt-equity ratio of 70:30, this translates into a €4-5 billion of funding capacity each year, which means 1-1.5GW per year. Thus, the funding gap.

Looking ahead

Given the macro-economic environment, multilaterals and ECAs will continue to be critical in the short to medium term but we expect the availability of construction finance to increase as the industry develops and standardises the bankability of the construction contracts. In the long run, we would expect commercial banks to provide mini-perm structured funding for the construction period and the early operation period, with a view to refinance post-construction through the capital markets.

The EIB’s 2020 Bond Initiative, aimed at enabling the structuring of project bonds and access to deeper pools of capital, is a welcome initiative. It may however take time for unwrapped project bonds to become readily accepted instruments and for the offshore sector to be able to package up investment-grade opportunities.

Much expectation is placed on participation from pension funds and insurance funds, which are looking to make sizeable direct investments in infrastructure assets that can provide long-term, stable, indexed-linked cashflows. They invest in individual infrastructure projects from their ‘alternatives’ capital allocations. As an asset class, infrastructure has been viewed favourably in recent years due to its apparent lack of correlation with volatile global equity and bond markets.

Infrastructure investment teams within these funds are relatively small and have large amounts of capital to deploy, so they tend to focus attention on a few large deals during their investment cycles. Given the global political capital invested in offshore wind, and the scale of the investment opportunities themselves, we do not see scale as a barrier to investment by these funds.

During the operational phase, supporters will argue that projects provide a relatively stable income stream to investors, which might be index-linked. These income streams should, theoretically, complement these funds’ long-term, index-linked liabilities. However, there are few, if any, projects that can prove to these risk-averse investors that the cashflow models stand the test of time.

Grid procurement

Delivering offshore transmission grid infrastructure in a timely fashion for connection can be particularly challenging in jurisdictions where the two activities are not actively managed by the same counterparty.

The industry has a constrained supply chain with limited supporting infrastructure — vessels, for example — and long lead times for major items. This means investment decisions need to be made far in advance of construction and possibly with no guarantee of the actual need for the proposed infrastructure. This can make programme management complex and costly, and delivery risky. There is significant potential for catastrophic events, such as weather-related delays during construction and damage to cable by shipping activity during operations. While these are insurable, they can lead to short-term cashflow deficits and delays.

The UK has successfully implemented the Offshore Transmission Operator regime, which forces post-construction refinancing of grid infrastructure projects away from the original developer/sponsor to financial institutions that can provide large pools of capital competitively under an investment-grade structure. This is allowing the recycling of capital to the original sponsors — mainly utilities — which can reinvest into another offshore wind project for example, while retaining control over delivery of transmission assets.

Countries such as Germany and Belgium are yet to develop a procurement mechanism that removes completion risks and does not put a significant financial weight on the local grid companies who are often regulated to deliver grid infrastructure. Meanwhile, a big part of the pipeline, in Germany in particular, is stranded for lack of transmission grid infrastructure.

The policy challenge

Europe’s offshore wind sector is at a crossroads. Regulatory and transmission infrastructure hurdles have slowed ‘growth’ momentum. Political leadership is required to drive changes and provide the stability to support investments in infrastructure and R&D.

The general consensus is that regulatory barriers relating to the delivery of the 2020 pipeline will eventually be addressed, unlocking a pipeline of projects. This will enable incumbents in particular to maintain a steady level of business activity but may not be sufficient to stimulate additional competition and bring the widely expected cost reduction. Driving a post-2020 vision for the sector should be high on the agenda of the European Commission but also of national governments if we want give the market the long-term visibility it requires to deliver.

Arnaud Bouillé is director and Kinga Duerrbaum is assistant director of Environmental Finance at Ernst & Young

.png)

.png)